Want to create or adapt books like this? Learn more about how Pressbooks supports open publishing practices.

1 Describe the language and environment of Canadian business.

Introduction

In this chapter, we will embark on a comprehensive journey through the fundamental aspects of business. We begin by defining basic business concepts, laying the groundwork for understanding the intricate world of commerce. Following this, we will delve into the various activities and environments that businesses operate within, providing a clear picture of the dynamic landscape. We will also explore the economic foundations that underpin business operations, and examine the critical forces of supply, demand, and competition that shape market behavior. Additionally, we will explain the cyclical nature of economies and the importance of productivity in sustaining growth. Finally, we will trace the evolution of the Canadian economy, highlighting key developments and trends that have shaped its current state.

Learning steps:

1.1 Define basic business concepts.

1.2 Review the activities and environment of business.

1.3 Summarize the economic foundations of business.

1.4 Describe the forces of supply, demand, and competition.

1.5 Explain economic cycles and productivity.

1.6 Describe the evolution of the Canadian economy.

1.1 Define basic business concepts.

Business, in its simplest form, is the practice of meeting people’s needs by offering products and earning a profit in return. A business can be a single person or a large organization, but its goal is always the same: provide something of value and receive financial reward—called profit—for doing so. The “product” a business offers may be a tangible good, such as a car, a smartphone, or a jacket. It can also be a service you cannot physically touch, like dry-cleaning, a medical check-up, or a concert. Sometimes the product is an idea—an accountant’s tax advice or an attorney’s legal strategy—meant to solve a problem rather than take up space on a shelf. Whatever shape it takes, a product must satisfy a customer’s need or desire if the business hopes to succeed.

Business: Individuals or organizations striving to earn profits by providing products that satisfy customers’ needs.

Profit: The financial reward from delivering products or services effectively.

Product: A good or service, tangible or intangible, that provides satisfaction and benefits.

Tangible Goods: Physical items like automobiles, smartphones, or clothing.

Services: Non-tangible offerings such as dry cleaning, medical consultations, or entertainment.

Ideas: Concepts or intellectual solutions, such as those provided by accountants or attorneys.

Beyond Profit: Nonprofits and Charities

Not every organization is built to earn profit. Nonprofits and charities exist to advance a mission or serve a cause, yet they still rely on many of the same business practices—budgeting, marketing, and strategic planning—to maximize their impact.

Stakeholders: Who They Are and Why They Matter

Whether an organization aims for profit or for social good, it operates within a web of relationships called stakeholders. Stakeholders are people or groups with an interest in how the organization performs and how its choices affect them.

Internal stakeholders work inside the organization. Owners—ranging from a single proprietor to shareholders of a public corporation—invest capital and expect a return or, in the case of public entities like Crown corporations or colleges, fulfill a public mandate. Employees contribute their time, knowledge, and effort to reach organizational goals and, in turn, rely on fair pay and a stable workplace.

External stakeholders stand outside the organization but are still influenced by its decisions—or can influence those decisions themselves. Customers buy or use the products and shape the business’s reputation through their satisfaction. Competitors vie for the same market, pushing each other to innovate. Policymakers and regulators set the rules of the game, ensuring safety, fairness, and compliance. Suppliers and distributors keep the supply chain moving so products reach customers on time. Bankers and investors provide the funds that help a business grow. Even the general public is a stakeholder, because a company’s social, environmental, and economic actions ripple through communities.

Long-term success depends on balancing the expectations of all these stakeholders. Ignoring any key group—whether it is employees, customers, or the wider community—can put the organization’s future at risk. By understanding who their stakeholders are and what they need, businesses and nonprofits alike can make better decisions, build stronger relationships, and achieve their goals more sustainably.

Key Insight: To succeed in the long run, businesses need to meet the needs and expectations of both internal and external stakeholders. If they neglect these groups, it can put the organization’s future at risk.

Internal Stakeholders

External Stakeholders

These individuals are directly involved in the organization’s day-to-day activities.

Owners: These can include sole proprietors, business partners, or shareholders in a corporation. In the case of public organizations like Crown corporations or colleges, ownership may rest with the government.

Employees: Employees are essential to any business. They contribute their time, skills, and effort to help the organization reach its goals.

These groups are not part of the business itself but are still affected by or can affect its operations.

Customers: They purchase or use the business’s goods or services and often influence demand and business reputation.

Competitors: Other businesses offering similar products or services compete for the same customers and market share.

Policy Makers and Regulators: Government bodies that create and enforce rules and regulations impacting how businesses operate.

Suppliers and Distributors: These are companies or individuals that provide the raw materials, products, or services a business needs to function and deliver to customers.

Bankers and Investors: They supply financial support, whether through loans, investments, or other funding mechanisms.

General Public: Communities and society at large can be affected by a business’s social, environmental, and economic impact.

Now, let’s examine a contemporary company that is rapidly transforming the way business is conducted.

What is OpenAI

OpenAI was founded in 2015 as a nonprofit organization by a group of influential entrepreneurs and researchers, including Elon Musk and Sam Altman. The company’s mission was to develop artificial intelligence (AI) that benefits humanity, with an initial $1 billion endowment that allowed it to focus on research and development without immediate financial pressures. However, in 2019, OpenAI transitioned from a nonprofit to a capped-profit model, establishing OpenAI LP. This structural shift enabled investment opportunities while maintaining some public-interest objectives. As a result, the company formed key partnerships, notably with Microsoft, which invested billions to integrate OpenAI’s technology into its platforms.

Ownership changes within OpenAI have been dynamic, reflecting the challenges of corporate governance in high-growth technology firms. Elon Musk, one of the original founders, departed in 2018 due to conflicts of interest. In November 2023, OpenAI faced significant internal turmoil when CEO Sam Altman was abruptly dismissed by the board, leading to widespread employee pushback and negotiations. This resulted in Altman’s reinstatement and a restructuring of the board of directors. These events underscore the complexities of leadership transitions, investor influence, and decision-making in the AI sector.

OpenAI’s product offerings center around advanced AI models and machine learning tools, providing services that enhance automation, content creation, and software development. Among its flagship products is ChatGPT, an AI-powered chatbot capable of generating human-like text for applications in research, content creation, and customer interactions. Another significant innovation is DALL·E, an AI system that generates images from text descriptions, catering to creative industries and marketing professionals. Additionally, OpenAI has developed Whisper, a speech recognition tool designed for transcribing and translating audio, and Codex, which assists programmers by generating and completing code in multiple programming languages.

Beyond these core products, OpenAI has expanded its offerings with specialized AI solutions. Custom GPTs allow businesses to develop AI models tailored to specific applications, while ChatGPT Enterprise provides corporate clients with enhanced AI functionality, improved data security, and customization options. These AI-driven tools target a broad range of industries, including education, marketing, software development, customer service, and healthcare, demonstrating the widespread applicability of OpenAI’s technologies.

OpenAI serves a diverse and expanding customer base across multiple sectors. Individual users, including students, researchers, and content creators, utilize ChatGPT for academic assistance, writing support, and brainstorming. Businesses and corporations integrate OpenAI’s models into their workflows to enhance automation, improve customer service, and streamline content generation. Software developers and technologists leverage AI tools like Codex to improve productivity and automate coding tasks, while media and marketing firms use AI-generated text and images for content creation and strategic decision-making.

One of OpenAI’s most significant partnerships is with Microsoft, which has incorporated OpenAI’s technology into products such as Bing, Edge, and Microsoft 365. This collaboration has expanded AI accessibility to millions of users worldwide, further cementing OpenAI’s role as a leading AI provider. As AI adoption continues to grow, OpenAI is well-positioned to serve both individual consumers and large-scale enterprise clients, reinforcing its influence in the global AI market.

Despite its origins as a nonprofit entity, OpenAI has significantly increased its revenue potential through its transition to a capped-profit model and strategic business partnerships. The company employs multiple revenue streams, including subscription-based services such as ChatGPT Plus and ChatGPT Enterprise, which offer premium AI features for a monthly fee. Additionally, OpenAI generates income through corporate licensing, allowing businesses to integrate its AI models into their proprietary systems for customized solutions. Partnerships and investments, particularly Microsoft’s multi-billion-dollar funding, provide OpenAI with financial support while enabling Microsoft to benefit from exclusive AI integrations.

Another revenue stream comes from the GPT Store and Custom GPTs, which allow users to create and monetize specialized AI models. This marketplace fosters an ecosystem where developers can contribute to AI advancements while generating income. However, OpenAI faces significant financial and operational challenges. AI development is resource-intensive, requiring substantial computing power, research funding, and compliance with evolving regulations. Furthermore, legal and ethical concerns, including copyright disputes and AI-generated misinformation, pose potential risks to OpenAI’s profitability and reputation. The company’s ability to navigate these challenges will be crucial in determining its long-term sustainability.

OpenAI’s evolution from a nonprofit research initiative to a dominant AI company illustrates key business concepts related to ownership, innovation, and market adaptation. Its diverse range of AI products and services caters to an expanding global customer base, reinforcing its influence across multiple industries. However, while OpenAI has demonstrated strong revenue potential through strategic partnerships and subscription models, it must also contend with financial, ethical, and regulatory challenges. Balancing innovation with responsible AI governance will be critical to OpenAI’s continued success in the rapidly evolving AI landscape.

How has the ownership of OpenAI changed over the years?

What are various revenue sources for the business?

Who are the customers of OpenAI LP?

What is the difference between For-profit, non-profit, and Limited-profit companies?

1.2 Review the activities and environment of business.

Why Business Matters

Businesses form the backbone of society, driving economies, creating jobs, and fulfilling societal needs. They contribute significantly to global progress, technological innovation, and economic interconnectivity, thereby improving our standard of living.

One of the key reasons businesses are essential is their role in innovation and technological progress. Entrepreneurs and businesses drive breakthroughs that shape the future, pushing the boundaries of what is possible and bringing new technologies to market. Job creation is another critical function of businesses. They provide employment opportunities that sustain livelihoods, offering people the means to support themselves and their families. Businesses also fuel economic growth. Through interconnected trade and financial systems, they stimulate both local and global economies, ensuring a continuous flow of goods, services, and capital.

Beyond financial contributions, businesses play a vital role in supporting communities. They enhance community stability and security, often engaging in initiatives that improve the quality of life for local residents. Workplaces foster social connection by providing environments where collaboration, networking, and a sense of belonging can thrive. These social interactions are crucial for personal and professional development. As societal needs evolve, businesses adapt to and anticipate changes in consumer demands. This ability to respond to evolving societal needs ensures that they remain relevant and continue to meet the needs of their customers. Through taxes, businesses contribute to funding public services. These funds support vital social programs and infrastructure, such as education, healthcare, and transportation systems.

Businesses also have a significant cultural influence. They create trends that shape societal values and lifestyles, impacting everything from fashion to technology to entertainment. Many businesses take on roles in advocacy and awareness, championing social justice and environmental causes. Their efforts can lead to positive changes in society and raise awareness about important issues. Finally, successful businesses serve as an inspiration for the future. They inspire the next generation of innovators and leaders, showing what is possible with hard work, creativity, and determination.

Businesses achieve their goals by organizing their employees into functional areas, each specializing in key tasks. These areas must work collaboratively, leveraging their unique strengths, to ensure the business thrives. The concept of synergy—where combined efforts yield greater results than individual contributions—illustrates the importance of integration. While each area may have its distinct focus, all must align to achieve the overarching goal: the success of the business.

Management: In any organization, managers are responsible for coordinating and guiding the work of employees across all areas of the business. Their main role is to ensure that the company is working efficiently and effectively toward its goals. To do this, managers carry out four key functions: planning what needs to be done, organizing resources and tasks, directing people to take action, and controlling processes to stay on track.

Human Resources: HR managers are responsible for ensuring that the organization has all of the skills and capabilities necessary to run the business. HR managers develop staffing plans, recruit and select new employees, monitor the performance management process, and develop succession plans for advancement and replacement. They develop standards for compensation and benefits and assist managers with staff issues.

Operations: All companies must convert resources (labour, materials, money, information, and so forth) into goods or services. Some companies, such as Apple, convert resources into tangible products—Macs, iPhones, etc. Others, such as hospitals, convert resources into intangible products — e.g., health care. The person who designs and oversees the transformation of resources into goods or services is called an operations manager. This individual is also responsible for ensuring that products are of high quality. In many organizations, operations management includes managing the supply chain which controls the delivery of raw materials and the distribution of finished goods.

Marketing: Marketing consists of everything that a company does to identify customers’ needs (i.e. market research) and design products to meet those needs. Marketers develop the benefits and features of products, including price and quality. They also decide on the best method of delivering products and the best means of promoting them to attract and keep customers. Marketing manages the relationship with customers and makes them aware of the organization’s desire and ability to satisfy their needs.

Accounting: Managers need accurate, relevant and timely financial information, which is provided by accountants. Accountants measure, summarize, and communicate financial and managerial information and advise other managers on financial matters. There are two fields of accounting. Financial accounting focuses on preparing financial statements to help users (both inside and outside the organization) assess the company’s financial health. Managerial accounting prepares information for internal use (for example, reports on the cost of materials in production) to assist in decision-making within the company.

Finance: Finance involves planning for, obtaining, and managing a company’s funds. Financial managers address such questions as the following: How much money does the company need? How and where will it get the necessary money? How and when will it pay the money back? What investments should be made in plant and equipment? How much should be spent on research and development? Good financial management is particularly important when a company is first formed because new business owners usually need to borrow money to get started.

Information Technology: Information is one of the most critical assets of most businesses today. Some businesses (such as social media companies) are entirely information-based. Information Technology (IT) managers are responsible for building computer and network infrastructures, implementing cybersecurity protocols, and developing user-facing software (like websites or apps for customers). There is often a high level of integration between a business’s IT systems and other departments such as finance, marketing, and operations. Businesses also frequently need to develop interfaces to send and receive information from other companies, including suppliers and logistics providers.

1.3 Summarize the economic foundations of business.

Economics can be understood as the study of how individuals, businesses, and societies make choices to satisfy their virtually unlimited wants with the limited resources available to them. At its heart, economics is about managing scarcity—making decisions about how best to allocate resources that are finite in nature but are required to fulfill needs and desires that are endless. These resources, commonly referred to as the Factors of Production, include land, labour, capital, and entrepreneurial ability.

Land refers to all natural resources that are used to produce goods and services, such as minerals, forests, water, and agricultural land. Labour encompasses all forms of human effort, both physical and mental, that contribute to the production process. Capital is not just money, but also includes tools, machinery, buildings, and other equipment necessary for production, as well as financial capital that supports these investments. Finally, entrepreneurial ability refers to the vision, innovation, and risk-taking required to combine the other resources effectively into new or improved products and services.

Entrepreneurs play a critical role in driving economic progress and innovation in Canada. Entrepreneurs are unique in their ability to combine resources to create goods and services that meet society’s needs. Entrepreneurs are more than just business owners; they are innovators and risk-takers. By investing their time, ideas, and resources, they create businesses that fuel economic growth. Their willingness to take calculated risks often results in the development of new technologies, improved services, and entirely new industries. In return, they reap the rewards of their efforts, whether through financial gain or the satisfaction of solving problems and creating impact. This entrepreneurial spirit forms the backbone of a dynamic economy, helping Canada remain competitive and adaptable in a rapidly changing global landscape.

How the resources are distributed and used varies across different economic systems, such as command economies, market economies, and mixed systems. Regardless of the system in place, every economy is faced with three fundamental questions that must be answered:

What goods and services should be produced?

How should these goods and services be produced, and by whom?

Who gets to consume them?

These questions shape the structure and behavior of the economy.

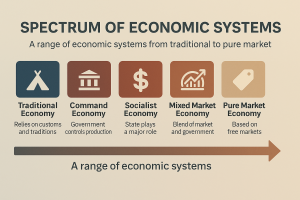

Types of Economic Systems

Traditional Economy: A traditional economy relies on long-standing customs, social roles, and communal sharing rather than formal markets or government planning. Production methods, trading partners, and even acceptable prices are inherited from previous generations, so economic change is slow and innovation is limited. Because output is usually aimed at subsistence, surpluses (and therefore cash) are rare. Example: Among the Maasai pastoralists of Kenya and Tanzania, cattle herding follows centuries-old migratory routes; wealth is measured in livestock, and meat or milk is bartered within the clan instead of sold in modern markets.

Command Economy (Planned Economy): In a command economy the state owns most productive resources and issues binding plans—often five- or ten-year blueprints—detailing what will be produced, in what quantity, and at what price. Wages, factory inputs, and even job assignments can be set by central ministries, leaving little room for private enterprise or consumer choice. Example: North Korea publishes annual quotas for staple crops, mines, and heavy industry. Citizens receive ration coupons for items as basic as rice or kerosene, and private commerce is officially restricted to small farmers’ markets tolerated on the margins.

Socialist Economy (State-led but Market-Aware): Under socialism, the government typically owns or strictly regulates “commanding heights” such as energy, transportation, health care, and banking, while permitting private ownership of smaller firms. Prices for essentials may be subsidized, and profits from state-owned enterprises are often redistributed through social programs. Example: China labels its system a “socialist market economy.” The state retains majority stakes in giants like Sinopec (energy) and ICBC (banking), sets ceilings on fuel and electricity prices, and guides investment through five-year plans, yet millions of privately owned restaurants, e-commerce shops, and tech start-ups compete freely for consumers.

Mixed Market Economy: A mixed‑market economy gives entrepreneurs substantial freedom to launch companies, hire employees, and set prices, while government oversight steps in to correct market failures and safeguard the public interest. Typical interventions include antitrust legislation, minimum‑wage laws, environmental regulations, and safety‑net programs such as unemployment insurance and public health care. For example, in Canada, business founders can enter almost any industry, provided they follow federal competition rules, provincial labour standards, and national product‑safety requirements. At the same time, the universally funded Medicare system guarantees access to doctors and hospitals, showing how public services can coexist with private enterprise.

Pure Market Economy (Theoretical Ideal): A pure market economy—sometimes called “laissez-faire capitalism”—would rest entirely on voluntary exchanges, with no taxes, subsidies, price controls, or regulatory agencies. Property rights would be enforced privately or through minimal courts, and all goods and services (including roads, money, and policing) would be bought and sold at market prices. Economists treat this as a useful thought experiment because every real nation, even the most pro-market, maintains some public services or rules to curb monopolies, protect consumers, or address inequality. Example (hypothetical): Imagine a digital island-state where all infrastructure is funded by user fees, contracts are policed by private arbitration firms, and citizens decide individually whether to purchase health insurance or schooling; no government body sets standards or redistributes income—an arrangement never fully achieved in practice.

Laissez-faire: A policy or attitude of letting things take their own course, without interfering.

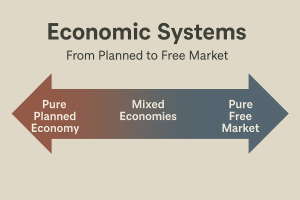

A nation’s economic system falls somewhere along a spectrum that ranges from planned to market‑driven. At one end of the spectrum lies a planned economy, where the state decides what to produce, in what quantities, and at what prices. Central planners set detailed output targets and price schedules, leaving firms and consumers with very little decision‑making power. At the opposite end is the pure free‑market economy, in which production and pricing are determined entirely by supply and demand.

Planned economies are often associated with communism, a political and economic ideology that seeks to eliminate class divisions by placing ownership of factories, mines, and other productive assets in the hands of the public. In theory, a communist society abolishes private property and money, distributing goods strictly according to need. While communism is not synonymous with central planning, communist states have typically relied on centrally planned mechanisms to implement their goals.

Socialism sits somewhat closer to the middle of the spectrum. Like communism, it favors public or state ownership of key industries; however, it allows for more private activity and often coexists with limited market forces. Because the government still directs large segments of production, most socialist systems are classified as planned (or at least partly planned) rather than market economies.

Moving further toward the market end is capitalism, where privately owned firms and individuals make production and pricing decisions. In its purest form—sometimes called laissez‑faire capitalism—the government plays a minimal role, allowing prices, wages, and output to adjust freely to changes in supply and demand.

The intellectual foundation for market capitalism was laid by Adam Smith, whose 1776 work The Wealth of Nations introduced the idea of the Invisible Hand. Smith argued that individuals who pursue their own self‑interest—hoping to earn profits or secure the best deal—unintentionally promote society’s welfare. Crucially, he noted that competition keeps this self‑interest in check: firms must improve quality and lower prices to attract buyers, while consumers (through their choices) ultimately determine which goods are produced. Taken together, self‑interest and competition generate the continuous adjustments that guide resources to their most valued uses.

Today, few countries operate at the extreme ends of the spectrum. Instead, most—including Canada—adopt a mixed economy that blends market signals with some level of government involvement. In any mixed or market‑oriented system, consumers wield significant influence. Their collective preferences, expressed through demand, signal which products and services hold value. Firms, motivated by potential profit, adjust supply to meet that demand, and competition among producers pushes them to allocate resources efficiently, keep prices in line, and innovate continuously. This ongoing interplay between limited resources and unlimited wants explains the trade‑offs that shape our daily choices—and the broader economy as well.

In Canada, privately owned businesses are free to decide what to produce and at what price, but the government provides essential services such as universal healthcare and regulates utilities like SaskPower and SaskTel. By contrast, the United States—also a mixed economy—leans slightly further toward market solutions, while European nations such as France maintain a stronger social‑welfare component.

In the next learning step, we will explore in depth how supply, demand, and competition interact within markets and why these forces remain central to modern economic life.

1.4 Describe the forces of supply, demand, and competition.

Demand for Goods and Services

Economists use the term demand to refer to the amount of some good or service consumers are willing and able to purchase at each price. Demand is fundamentally based on needs and wants—if you have no need or want for something, you won’t buy it. While a consumer may be able to differentiate between a need and a want, from an economist’s perspective they are the same thing. Demand is also based on ability to pay. If you cannot pay for it, you have no effective demand. By this definition, a person who does not have a drivers license has no effective demand for a car.

What a buyer pays for a unit of the specific good or service is called price. The total number of units that consumers would purchase at that price is called the quantity demanded. A rise in price of a good or service almost always decreases the quantity demanded of that good or service. Conversely, a fall in price will increase the quantity demanded. When the price of a gallon of gasoline increases, for example, people look for ways to reduce their consumption by combining several errands, commuting by carpool or mass transit, or taking weekend or vacation trips closer to home. Economists call this inverse relationship between price and quantity demanded the law of demand. The law of demand assumes that all other variables that affect demand (which we explain in the next module) are held constant.

Supply of Goods and Services

When economists talk about supply, they mean the amount of some good or service a producer is willing to supply at each price. Price is what the producer receives for selling one unit of a good or service. A rise in price almost always leads to an increase in the quantity supplied of that good or service, while a fall in price will decrease the quantity supplied. When the price of gasoline rises, for example, it encourages profit-seeking firms to take several actions: expand exploration for oil reserves; drill for more oil; invest in more pipelines and oil tankers to bring the oil to plants for refining into gasoline; build new oil refineries; purchase additional pipelines and trucks to ship the gasoline to gas stations; and open more gas stations or keep existing gas stations open longer hours. Economists call this positive relationship between price and quantity supplied—that a higher price leads to a higher quantity supplied and a lower price leads to a lower quantity supplied—the law of supply. The law of supply assumes that all other variables that affect supply (to be explained in the next module) are held constant.

Demand curve

Supply curve

Demand curves will appear somewhat different for each product. They may appear relatively steep or flat, or they may be straight or curved. Nearly all demand curves share the fundamental similarity that they slope down from left to right. Demand curves embody the law of demand: As the price increases, the quantity demanded decreases, and conversely, as the price decreases, the quantity demanded increases. Similarly, the shape of supply curves will vary somewhat according to the product: steeper, flatter, straighter, or curved. Nearly all supply curves, however, share a basic similarity: they slope up from left to right and illustrate the law of supply: as the price rises the quantity supplied increases. Conversely, as the price falls, the quantity supplied decreases.

Equilibrium—Where Demand and Supply Intersect

Because the graphs for demand and supply curves both have price on the vertical axis and quantity on the horizontal axis, the demand curve and supply curve for a particular good or service can appear on the same graph. Together, demand and supply determine the price and the quantity that will be bought and sold in a market.

Figure below illustrates the interaction of demand and supply in the market for gasoline.

Remember this: When two lines on a diagram cross, this intersection usually means something. The point where the supply curve (S) and the demand curve (D) cross, designated by point E is called the equilibrium. The equilibrium price is the only price where the plans of consumers and the plans of producers agree—that is, where the amount of the product consumers want to buy (quantity demanded) is equal to the amount producers want to sell (quantity supplied). Economists call this common quantity the equilibrium quantity. At any other price, the quantity demanded does not equal the quantity supplied, so the market is not in equilibrium at that price.

The equilibrium price is $1.40 per gallon of gasoline and the equilibrium quantity is 600 million gallons. If you had only the demand and supply schedules, and not the graph, you could find the equilibrium by looking for the price level on the tables where the quantity demanded and the quantity supplied are equal.

The word “equilibrium” means “balance.” If a market is at its equilibrium price and quantity, then it has no reason to move away from that point. However, if a market is not at equilibrium, then economic pressures arise to move the market toward the equilibrium price and the equilibrium quantity.

If the price of a gallon of gasoline was above the equilibrium price—that is, instead of $1.40 per gallon, the price is $1.80 per gallon, the dashed horizontal line at the price of $1.80 illustrates this above-equilibrium price. At this higher price, the quantity demanded drops from 600 to 500. This decline in quantity reflects how consumers react to the higher price by finding ways to use less gasoline. Moreover, at this higher price of $1.80, the quantity of gasoline supplied rises from 600 to 680, as the higher price makes it more profitable for gasoline producers to expand their output. Now, consider how quantity demanded and quantity supplied are related at this above-equilibrium price. Quantity demanded has fallen to 500 gallons, while quantity supplied has risen to 680 gallons. In fact, at any above-equilibrium price, the quantity supplied exceeds the quantity demanded. We call this an excess supply or a surplus.

With a surplus, gasoline accumulates at gas stations, tanker trucks, pipelines, and oil refineries. This accumulation puts pressure on gasoline sellers. If a surplus remains unsold, those firms involved in making and selling gasoline are not receiving enough cash to pay their workers and to cover their expenses. In this situation, some producers and sellers will want to cut prices, because it is better to sell at a lower price than not to sell at all. Once some sellers start cutting prices, others will follow to avoid losing sales. These price reductions in turn will stimulate a higher quantity demanded. Therefore, if the price is above the equilibrium level, incentives built into the structure of demand and supply will create pressures for the price to fall toward the equilibrium.

Suppose the price is below its equilibrium level at $1.20 per gallon, as the dashed horizontal line. At this lower price, the quantity demanded increases from 600 to 700 as drivers take longer trips, spend more minutes warming up the car in the driveway in wintertime, stop sharing rides to work, and buy larger cars that get fewer miles to the gallon. However, the below-equilibrium price reduces gasoline producers’ incentives to produce and sell gasoline, and the quantity supplied falls from 600 to 550. When the price is below equilibrium, there is excess demand, or a shortage—that is, at the given price the quantity demanded, which has been stimulated by the lower price, now exceeds the quantity supplied, which has been depressed by the lower price. In this situation, eager gasoline buyers mob the gas stations, only to find many stations running short of fuel. Oil companies and gas stations recognize that they have an opportunity to make higher profits by selling what gasoline they have at a higher price. As a result, the price rises toward the equilibrium level.

Types of Market Competition

Market Structure

Characteristics

Examples

Perfect Competition

Many buyers and sellers offer virtually identical (standardized) products. Price is the only differentiating factor, and no single buyer or seller can influence it (each is a “price taker”).

Agricultural markets for staple goods (e.g., wheat, corn) or commodities like crude oil in a global market.

Monopolistic Competition

Many sellers offer differentiated products that are similar but not identical. Businesses compete on product quality, style, brand, or convenience in addition to price. Each firm has a small degree of market power due to uniqueness of its product.

Restaurants, clothing brands, and consumer electronics companies (each offers a slightly different product experience).

Oligopoly

A few large sellers dominate the market, each holding a significant market share. High barriers to entry (like huge startup costs or complex technology) limit the number of competitors. Firms may collude or follow each other’s lead on pricing and output decisions.

Automobile manufacturers, commercial airlines, and big banks are industries often characterized as oligopolies.

Monopoly

A single seller controls the entire market for a product or service, with no close substitutes available. Because the firm faces no competition, it can exert significant control over prices. (True monopolies are rare and often subject to government regulation.)

Public utilities in a region (e.g., electricity distribution) are often natural monopolies. A patented prescription drug is a legal monopoly for the patent holder during the patent period.

In monopolistic competition, marketing plays a crucial role in highlighting product differences and justifying higher prices for unique features. In an oligopoly, firms have some ability to set prices but must always consider competitors’ reactions (for example, if one major bank lowers its mortgage rates, others will likely follow suit). Some monopolies can be natural monopolies (industries like electricity distribution, where the infrastructure costs make competition impractical; these are usually regulated by the government to ensure fair pricing and universal access) or legal monopolies (monopolies granted by law, such as patents that give a company exclusive rights to produce a new product for a certain period, allowing it to recover research and development costs).

The majority of consumer products fall under monopolistic competition, where differentiation is key to market success. Understanding how supply, demand, and competition intersect in these market structures is vital to grasping the dynamics of a mixed market economy.

1.5 Explain economic cycles and productivity.

Understanding the Canadian Economy: Every day, we are inundated with economic news—be it on television, online, or through discussions in class. Topics such as the economy’s performance (measured by GDP), unemployment rates, inflation, housing prices, government debt, and consumer confidence trends dominate the headlines. For students studying business and aspiring to become business owners or managers, understanding these key concepts is essential.

The Canadian economy is influenced by numerous factors, and the government plays a pivotal role in shaping its direction. This learning step introduces fundamental economic concepts to help you navigate and make sense of the information surrounding you. While you might delve deeper into these ideas in a macroeconomics course later, this summary will provide you with a foundational understanding.

Key Concepts in the Canadian Economy

Gross Domestic Product (GDP) One of the most important measures of an economy’s performance is Gross Domestic Product (GDP), which represents the market value of all goods and services produced domestically in a given year. The GDP is defined as the market value of all goods and services produced by the economy in a given year. The GDP includes only those goods and services produced domestically; goods produced outside the country are excluded. The GDP also includes only those goods and services that are produced for the final user; intermediate products are excluded.

What counts: Only goods and services produced for the final user. Intermediate products, like components used in manufacturing, are excluded. For example, the silicon chip that goes into a computer (an intermediate product) would not count directly because it is included when the finished computer is counted.

Why it matters: By itself, the GDP doesn’t necessarily tell us much about the direction of the economy. But change in the GDP does. If the GDP (after adjusting for inflation, which will be discussed later) goes up, the economy is growing. If it goes down, the economy is contracting. There is some debate amongst economists that GDP provides the most accurate measure of an economy’s performance.

The business cycle refers to recurring fluctuations in real GDP over time, characterized by four phases:

Peak: The highest point before economic contraction.

Recession: A period of economic decline.

Trough: The lowest point before recovery begins.

Expansion: A period of economic growth.

Healthy, long-term growth trends are essential for improving standards of living and fostering societal well-being.

Watch this video for an overview of the business cycle.

Economists often argue that GDP per capita—total national output divided by the population—is a clearer gauge of economic well‑being than overall GDP.

A second barometer of economic health is the unemployment rate, the share of the labor force that is jobless and actively seeking work. In Canada, economists regard “full employment” as roughly six percent unemployment, a level that accommodates normal seasonal shifts and people temporarily between jobs.

A third key indicator is inflation, the general rise in prices over time. Moderate, predictable inflation signals a growing economy and encourages spending and investment. By contrast, rapid inflation erodes purchasing power, while deflation (falling prices) can prompt consumers to delay purchases, both of which can stall economic growth.

Federal Debt and Its Implications: The government funds its expenditures through taxes or by borrowing. When annual spending exceeds revenue, the government incurs a budget deficit, contributing to the overall federal debt.

Why it matters: Interest on this debt is paid through tax dollars, and large deficits can indicate economic vulnerabilities.

A well-functioning economy enables higher standards of living, better healthcare, and more opportunities for leisure and personal fulfillment. Businesses, especially in Canada’s globalized market, are at the heart of this system, driving growth and innovation.

Governments typically strive to achieve three major economic goals simultaneously:

Steady GDP Growth – Consistent, sustainable economic growth (increases in GDP) is critical for job creation, higher standards of living, and a thriving business environment. Low Unemployment – Maintaining a low unemployment rate (near the “full employment” level) ensures that labor resources are being efficiently utilized and contributes to social stability. Stable Prices (Low, Predictable Inflation) – Keeping inflation low, steady, and predictable helps maintain a stable economy where individuals and businesses can plan for the future without worrying about erratic price changes.

Federal Debt and Its Implications: The government funds its expenditures through taxes or by borrowing. When annual spending exceeds revenue, the government incurs a budget deficit, contributing to the overall federal debt.

Why it matters: Interest on this debt is paid through tax dollars, and large deficits can indicate economic vulnerabilities.

A well-functioning economy enables higher standards of living, better healthcare, and more opportunities for leisure and personal fulfillment. Businesses, especially in Canada’s globalized market, are at the heart of this system, driving growth and innovation.

1.6 Describe the evolution of the Canadian economy.

Canada’s economy has evolved significantly over time, transitioning through distinct phases that reflect societal, technological, and industrial advancements. These phases demonstrate how economic structures adapt to meet changing needs and opportunities.

The Early Economy: In its earliest phase, Canada’s economy was largely agricultural. Colonists established self-sufficient communities, producing almost everything they needed locally. This traditional economy emphasized subsistence and minimal trade, reflecting the “traditional economy” model discussed in our previous lessons.

The Industrial Revolution: The Industrial Revolution marked a transformative period for Canada’s economy. The introduction of machinery and job specialization increased production speed and efficiency. This era laid the foundation for large-scale industrialization, reshaping labor and economic structures.

The Manufacturing Economy: Industrialization ushered in a manufacturing economy, focusing on the mass production of goods and services. Factories became central to economic activity, providing employment and driving urbanization across Canada.

The Marketing Economy: As businesses grew, they began prioritizing consumer needs and desires. This led to the marketing economy, where companies tailored products and services to meet market demands. The focus shifted from mere production to understanding and fulfilling consumer expectations.

The Service Economy: Post-World War II economic prosperity introduced the service economy. Rising incomes and improved quality of life enabled people to hire others for various services. This period also saw a significant increase in women joining the workforce, further fueling the demand for professional and personal services.

The New Digital Economy: The emergence of advanced technology and digital media catalyzed the new digital economy. E-commerce platforms like Amazon transformed how goods and services are bought and sold. Digital innovations continue to create new products and services, fundamentally changing industries and consumer behaviors.

Artificial Intelligence (AI): The newest phase of economic evolution is powered by artificial intelligence (AI), which allows machines to perform tasks that once demanded human intelligence and is already reshaping business operations. AI‑driven analytics handle massive volumes of structured and unstructured data—so‑called “big data”—at unprecedented speeds, uncovering insights that guide strategy and innovation. Blockchain technology, another AI‑enabled advance, provides a tamper‑resistant, decentralized ledger that enhances data security and builds trust across supply chains and financial transactions. Meanwhile, AI‑guided drones are taking on roles such as product delivery, aerial surveying, and environmental monitoring in sectors ranging from construction and agriculture to defense and retail. Although these breakthroughs boost productivity and service quality, they also raise ethical questions about privacy, decision transparency, and job displacement, forcing organizations and workers alike to adapt to a rapidly changing economic landscape.

Conclusion

By now, you have an understanding of the essential elements that constitute the business world. You are equipped with knowledge about basic business concepts, the activities and environments in which businesses thrive, and the economic principles that drive business decisions. You also have a clear grasp of how supply, demand, and competition influence markets, and the significance of economic cycles and productivity in economic health. Moreover, you appreciate the historical context and evolution of the Canadian economy, providing a broader perspective on how past events and trends inform present-day economic conditions. This foundational knowledge serves as a crucial stepping stone for more advanced studies in business and economics.

1.7 LO1 – Business Case

First, you decide whether you will work individually or in a team. Then, you will begin your work by applying course concepts covered in this Learning Outcome to an existing business of your choice.

![The business cycle, also known as the economic cycle or trade cycle, is the downward and upward movement of gross domestic product (GDP) around its long-term growth trend.[1] The length of a business cycle is the period of time containing a single boom and contraction in sequence. These fluctuations typically involve shifts over time between periods of relatively rapid economic growth (expansions or booms), and periods of relative stagnation or decline (contractions or recessions). Business cycles are usually measured by considering the growth rate of real gross domestic product. Despite the often-applied term cycles, these fluctuations in economic activity do not exhibit uniform or predictable periodicity.](https://www.saskoer.ca/app/uploads/sites/179/2025/02/2-BusinessLifeCycle-Graph-1024x707.png)