9 Accounts Receivable

NRV and the Allowance Method

Basic A/R entries

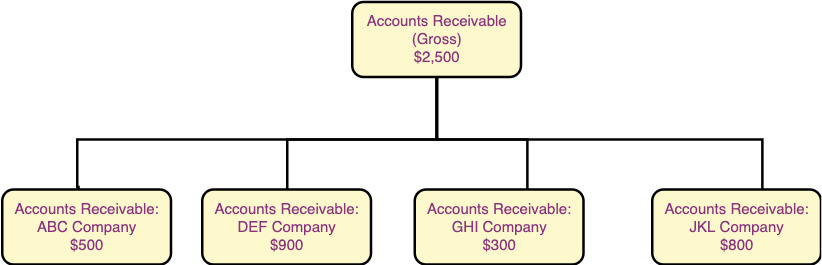

So far we have discussed the A/R account balance, looking at A/R as simply an account on the Statement of Financial Position. But A/R is actually the total, or summation, of many individual accounts owing by customers. These individual accounts allow companies keep track of how much each of their customers owe them, which is super useful when a customer calls to find out how much they owe. So although we record our journal entries using the generic “A/R” account in class, the accounting system actually looks more like this:

Tell Me More

When accountants say on account, it just means using accounts receivable. The customer did not pay for them at the time of sale but will pay later. You will see the phrase on account often in this textbook because it is used frequently in practice.

And in real life, you will record the customer account when making any journal entry to A/R. Look at the flowchart above: A/R gross holds the total balance owed from all customers of $2,500, calculated as $500 + $900 + $300 + $800. This $2,500 balance owing is shown on the Statement of Financial Position as A/R (gross).

This will be important later, so please take note: A/R (gross) is the total amount owed by all customers; a simple accumulation of all customer accounts.

![]()

Before we go any further, let’s pause and enjoy some practice with A/R journal entries. The following examples include sale transactions and repayment of customer accounts. I’ll do the first example, and you do the second!

- My Turn:

- Sal-T-Dog Ltd. is a wholesaler that sells pet supplies. In June 20X8, Sal-T-Dog had the following transactions. Record all necessary journal entries for each transaction (ignore sales taxes).

- 1 June:

- Sal-T-Dog sold 80 dog beds on account to a retailer called Malty Corp for $40/bed (cost: $15/bed).

-

(to record sale of dog beds to Malty Corp on account [80 beds × $40 ⁄ bed]) DR A/R (Malty Corp) 3,200 CR Sales Revenue 3,200 (to record inventory reduction upon sale of dog beds [80 beds × $15 ⁄ bed]) DR Cost of Goods Sold 600 CR Inventory 600 - 5 June:

- Sal-T-Dog sold 40 dog leashes on account to a new customer, PetsMatter Inc., for $200 (cost: $90).

-

(to record sale of dog leashes to PetsMatter on account) DR A/R (PetsMatter Inc.) 200 CR Sales Revenue 200 (to record inventory reduction upon sale of dog leashes) DR Cost of Goods Sold 90 CR Inventory 90 - 15 June:

- Malty Corp paid $1,250 to Sal-T-Dog as partial repayment on account.

-

(to record collection of A/R) DR Cash 1,250 CR A/R (Malty Corp) 1,250

![]()

Now it’s your turn. Continue the example of Sal-T-Dog – give it a try!