2 Assets and Liabilities

Statement of Financial Position Fundamentals

Liabilities

![]()

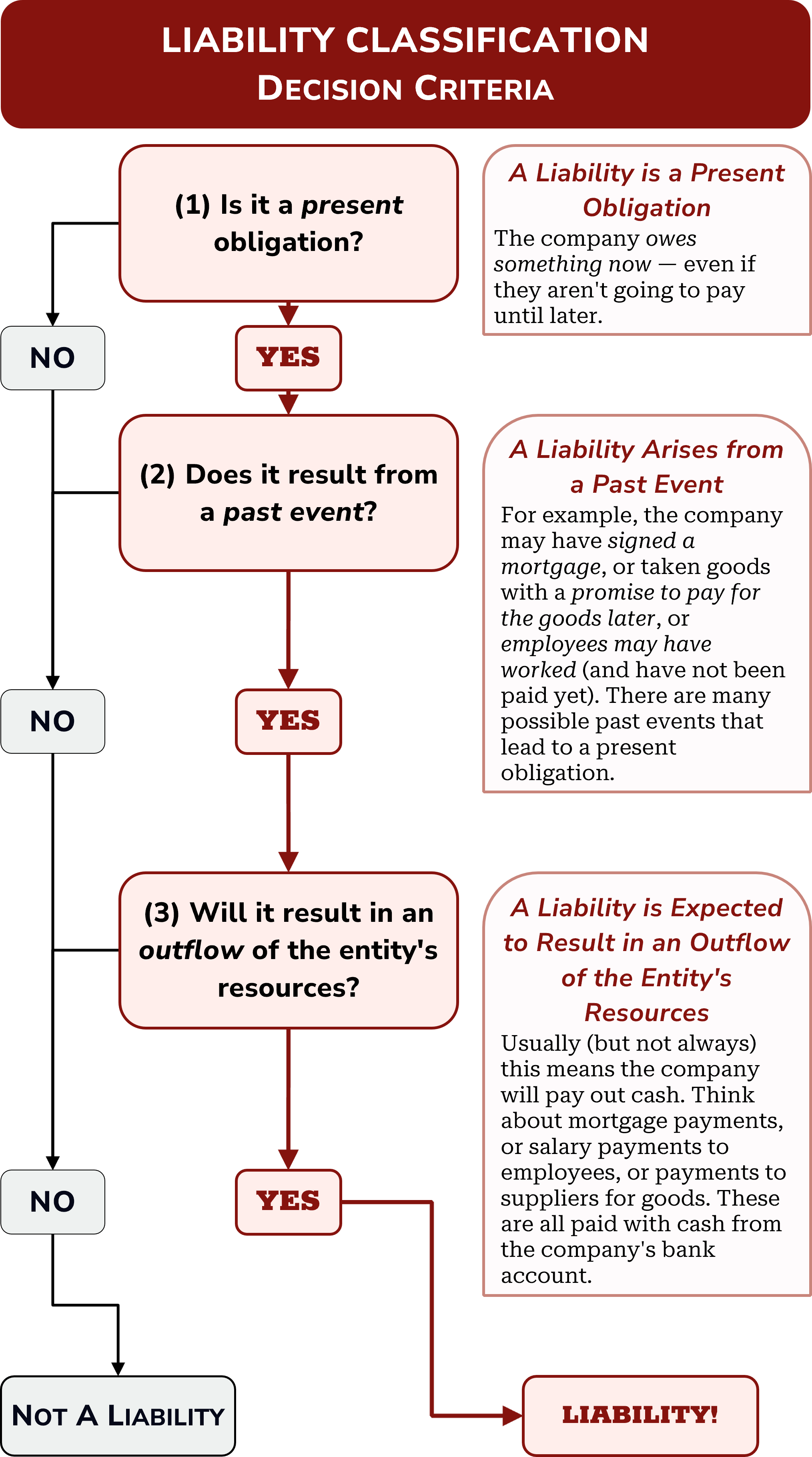

The technical definition of a liability is: (a) a present obligation of the entity (b) arising from past events, the settlement of which is (c) expected to result in an outflow of the entity’s resources.

If we go back to the simple definition—an asset is what you own—then a liability is just the opposite: a liability is what you owe. A company may owe money in the form of borrowings (for example, for T-shirts you picked up but haven’t paid for yet, or a mortgage on a building). Or a company may owe money to employees for time worked (accrued wages).

Or maybe a company owes customers custom T-shirts because a customer has paid a deposit (Unearned RevenueUnearned Revenue:

A current liability account that holds cash payments until revenue is earned. Typically, these are deposits paid by customers for future sales or services. The journal entry to increase unearned revenue is DR Cash and CR Unearned revenue. When revenue is earned, unearned revenue decreases as DR Unearned revenue and CR sales revenue.). There are many possibilities because a company can be obligated for many different reasons. Below is a flowchart for liabilities. Consider a potential liability like a credit card balance owing. Is it a liability? Answer the questions below and follow the arrows to find out.

Classifying Liabilities: A Helpful Flowchart

![]()

What did you find? Is a credit card balance a liability? Let’s take a look:

| Decision Criteria | Discussion | Criterion Met? |

|---|---|---|

| Is a credit card balance a present obligation? | A credit card balance will have to be paid back. It is therefore a present obligation. We owe the credit card company now, even if we don’t pay off our credit card immediately. |  |

| Does a credit card balance result from a past event? | The credit card balance increased somehow. The entity made purchases and used the credit card to pay for them. | |

| Will a credit card balance result in an outflow of the entity's resources? | The credit card company will require a payment from the entity. The entity will pay in cash, a resource. | |

Here’s another example. Graphics Co. creates graphic designs on t-shirts. They took out a bank loan to purchase machinery. Is this loan a liability?

| Decision Criteria | Discussion | Criterion Met? |

|---|---|---|

| Is the loan a present obligation | The loan balance will have to be paid back to the bank. Graphics Co owes the bank now, but will pay the loan back in regular instalments. | |

| Does the loan result from a past event? | Graphics Co. borrowed money from the bank—a past event. | |

| Will the loan result in an outflow of the entity's resources? | Graphics Co. will pay back the loan in instalments over time. They will pay cash which is a resource belonging to Graphics Co. | |

![]()

So now you know that assets are what a company owns and a liability is what a company owes. You have been given 3-part decision criteria (in the form of definitions) for assets and liabilities. Now let’s practice identifying items as assets and liabilities.

The answers are embedded within the spreadsheet—but don’t look at them until you’ve tried each item. Accounting is not a spectator sport—the only way to learn this is to practice!